Jumeirah Village Circle is the district most people learn about second when they start looking at Dubai apartment investment. The first is usually Dubai Marina or Downtown, which they ruled out because the entry prices were too high. JVC is where the math suddenly starts to feel possible. Studios under half a million. One-bedrooms in the AED 700,000 range. Yields advertised at 8% plus. Payment plans. Foreign-friendly. Mortgage-friendly.

Most of those headline numbers are still accurate in 2026. But the underlying picture has shifted enough over the past three years that the JVC investment thesis today is meaningfully different from the JVC investment thesis in 2022 or 2023. Some changes are good for investors. Some are not. The honest case for JVC in 2026 requires unpacking what’s actually changed.

The big shifts. JVC has more residents now than at any point in its history. The area is no longer the half-built construction zone it was even five years ago. The retail nodes work. The schools have opened. The road network has improved. All of that is good for tenant demand and for owner-occupier appeal. The flip side: capital growth has compressed because the area is now broadly priced for the maturity it has reached. The easy gains from buying in 2020 and watching the area fill in are gone. What replaces them is a more conventional yield-and-modest-growth profile that sits closer to JLT than to Dubai South on the risk-and-return spectrum.

We’ve handled JVC investment transactions across most of its districts and we’ve watched the patterns play out in real portfolios. This article is the data-led version of the conversation we have with most JVC buyers. What yields actually deliver in 2026 versus what they advertise. Which clusters and buildings perform versus which look good on paper. What capital growth has done and is likely to do. Where the risks have shifted. And the honest read on whether JVC still works for the kind of investor reading this piece.

A note before getting in. JVC is no longer a frontier district. The early-mover thesis (buy in 2018, ride the build-out, exit by 2025) has largely played out. What JVC offers in 2026 is more conventional. Decent yields, mature tenant pool, moderate capital appreciation, deep secondary liquidity. For the right kind of investor, that conventional profile is exactly what they want. For investors looking for the next frontier, JVC is now an established asset class rather than a growth bet.

JVC in 2026: What’s Changed

JVC sits between Al Khail Road and Sheikh Mohammed bin Zayed Road, roughly equidistant from Marina and the centre of new Dubai. The area is structured around 11 districts (1 through 11), each with a mix of mid-rise apartment buildings, townhouses, and a few villa clusters. The development started taking serious shape in the late 2010s and reached meaningful build-out around 2022-2023.

What has changed in the past three years that matters for investors:

• Tenant pool depth has roughly doubled. The area now has more than 100,000 residents and the rental market clears quickly even outside peak seasons

• Retail nodes at Circle Mall and various community centres are now operational and well-trafficked

• Schools including Sunmarke and JSS International have established themselves and pull family tenants

• Service charges have stabilised across most buildings as reserve funds have caught up to maintenance needs

• Resale market liquidity has deepened materially. Secondary transactions in JVC now clear at competitive timelines comparable to JLT

• Supply pipeline has cooled compared to the 2020-2022 peak, though selected off-plan launches continue

• Quality variance across buildings has narrowed somewhat as the worst-built early supply has either been refurbished or has rented at a clear discount that the market has priced in

These shifts together have moved JVC from a frontier district to a mature mid-tier district. The implications for investment are real.

Lewis Allsopp, founder of Allsopp & Allsopp, has spoken publicly about how JVC’s rental dynamics have evolved through the 2020s. The pattern he describes broadly matches what we see in our own transaction data. Demand is sticky. Supply is moderating. The wide variance between premium and basic stock within JVC has narrowed without disappearing.

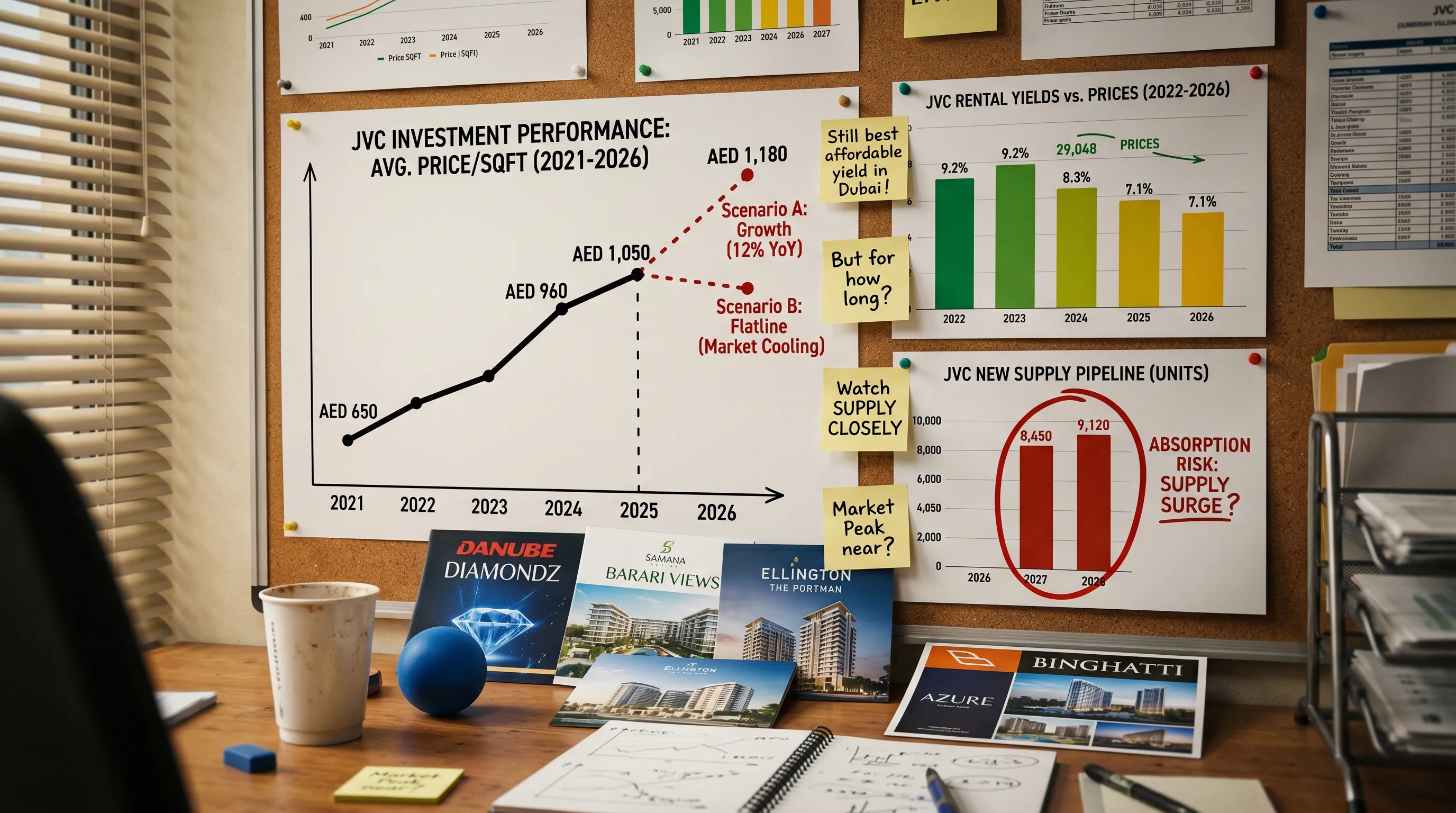

The 2026 JVC Yield Trajectory

Gross rental yields in JVC currently run between 7.2% and 9.0% depending on cluster, building age, and unit type. The median across the area sits around 7.8%. That puts JVC clearly ahead of central Dubai apartment yields (5.5% to 6.5%) and roughly in line with JLT (around 7.1%) and Dubai South (around 7.5%). It sits below Dubailand older stock (8% to 10%) but with better build quality and infrastructure depth.

Net yields after service charges, agent fees, and typical voids run 6.0% to 7.5% across most JVC buildings. The gap between gross and net is wider in some older buildings with higher service charges relative to rent, and narrower in newer buildings where rents have caught up to the service charge bill.

Rental growth in JVC between 2022 and 2025 ran between 55% and 75% depending on cluster, which is at the upper end of the Dubai apartment market. The big moves came in 2022 and 2023 as the post-pandemic demand surge played out. 2024 and 2025 have seen slower but still positive rental growth, with most JVC clusters posting 5% to 12% annual rental increases.

Capital appreciation between 2022 and 2025 ran around 40% across JVC on average, broadly in line with the city-wide apartment average of 45%. The strongest growth came in clusters near Circle Mall and the better-located districts. The weaker growth came in the older outlying districts and buildings with documented maintenance issues.

Taimur Khan, CBRE’s research head for the Middle East, has noted that JVC’s relative yield premium over central Dubai has narrowed slightly through 2024 and 2025 as rents in central districts caught up to JVC’s growth. That narrowing matters for the investment case. JVC’s yield advantage over the rest of the market is real but smaller than the headline numbers suggest after you account for void rates, service charge variance, and the specific buildings in question.

A useful frame for thinking about JVC yields in 2026:

1. Headline gross yields of 8% to 9% are achievable in specific buildings and clusters but not across the average

2. Realistic portfolio yields after all costs land between 6.0% and 7.5% for most investors

3. The yield premium over JLT and central Dubai has narrowed to roughly 1 to 2 percentage points net

4. Building selection matters more than cluster selection. Two units in the same JVC district can yield 1.5 percentage points apart based on building management and finish quality

5. Void rates in JVC are now comparable to JLT for well-managed buildings, around 2 to 4 weeks between tenants

Which JVC Clusters and Buildings Actually Perform

JVC is structured around 11 districts. Some have outperformed materially. Others have lagged. The breakdown:

District 10 and District 11, the newer northern clusters closer to Al Khail Road, have delivered the strongest combination of yield and capital growth over the past three years. Build quality is generally better. Buildings are newer. Rents have grown faster.

Circle Mall vicinity (Districts 12 and 13), with strong retail proximity, has held up well on both yield and resale velocity. Tenant demand is consistently strong here.

District 14 and the southern clusters have been moderate performers. Yields are healthy but capital growth has lagged the JVC average slightly.

The older inner districts (Districts 1 through 5) carry the most variance. Some buildings here are excellent value with strong yields. Others have aged poorly and rent at noticeable discounts. Walking the building before purchase is essential.

Specific buildings worth flagging based on consistent performance:

1. Belgravia Heights series in District 12 and 13, by Ellington. Strong build quality, reliable rental performance, consistent service charge management

2. Bloom Heights in District 11, a popular two-tower complex with consistent occupancy

3. Pantheon Boulevard, an older building that has aged well with stable service charges

4. The various Imtiaz developments scattered across JVC, generally well-managed with predictable yields

5. Tonino Lamborghini Residences, one of the newer branded developments with premium pricing and stronger capital growth profile

6. Park View by Azizi, mid-tier with reliable rental absorption

7. Eaton Place, an established mid-tier building with one of the more consistent track records in JVC

8. Several JVC Tilal communities for those interested in townhouse-adjacent apartment supply

Buildings to verify before buying:

1. Several smaller early-vintage buildings from 2015-2017 era with documented maintenance deferral

2. Any building where the owners’ association is in dispute over service charges

3. Buildings with high investor-owner concentration (above 80%) and limited owner-occupier presence, which can create governance issues

4. Buildings near construction sites where the immediate environment may change materially over the next 2-3 years

These aren’t absolute rules but they’re patterns we’ve watched repeat. The team can pull the specific building data before any purchase commitment.

Capital Growth in JVC and Where It’s Headed

JVC’s capital appreciation story has matured. The 50%-plus three-year capital gains we saw in some clusters between 2020 and 2023 are unlikely to repeat from current price levels. What replaces them is a more conventional growth profile.

Faisal Durrani, Knight Frank’s head of Middle East research, has consistently flagged JVC’s evolution from frontier to mainstream Dubai apartment district. The implication for capital growth is that JVC should now track broader Dubai apartment averages rather than significantly outperform them. That’s not a bearish call. It’s a recognition that the area has matured.

Looking forward over a 3 to 5 year hold:

The base case scenario has JVC apartment values growing at 4% to 7% annually in nominal terms, broadly in line with Dubai apartment market trend. That gives total cumulative growth of roughly 20% to 40% over a 5-year hold. Combined with 6% to 7.5% net yields, that’s a credible 11% to 14% total annual return for the period.

The bull case has JVC continuing to benefit from broader Dubai market strength, with capital growth running 8% to 10% annually and total returns approaching 15% to 17% per year. This requires the broader Dubai market to maintain its current momentum, which is plausible but not guaranteed.

The bear case has JVC capital values flat or modestly down for 1-2 years as supply catches up to demand, with yields holding up. That gives total returns of 5% to 7% annually for the period. This is the floor scenario most investors should stress-test against.

None of these scenarios are extreme. The variance is narrower than for districts at the frontier (like Dubai South) or districts highly exposed to specific demand drivers (like City Walk’s lifestyle premium). That predictability is part of JVC’s current appeal.

Our Research on JVC Apartment Performance

We pulled data on roughly 130 JVC transactions and 220 rental contracts from 2023 and 2024, drawing from our records and Property Monitor. The cluster-by-cluster breakdown:

Studios in older buildings (Districts 1-5), average price AED 460,000, average rent AED 41,000. Gross yield: 8.9%.

Studios in newer buildings (Districts 10-13), average price AED 540,000, average rent AED 45,000. Gross yield: 8.3%.

One-bedrooms in older buildings, average price AED 720,000, average rent AED 60,000. Gross yield: 8.3%.

One-bedrooms in newer mid-tier buildings, average price AED 850,000, average rent AED 70,000. Gross yield: 8.2%.

One-bedrooms in premium/branded buildings (Tonino Lamborghini, Belgravia, etc), average price AED 1.15 million, average rent AED 86,000. Gross yield: 7.5%.

Two-bedrooms in mid-tier JVC buildings, average price AED 1.4 million, average rent AED 110,000. Gross yield: 7.9%.

Two-bedrooms in premium JVC buildings, average price AED 1.85 million, average rent AED 130,000. Gross yield: 7.0%.

Three-year capital growth by cluster, 2022 to 2025:

Districts 1-5 (older inner): 32%. Districts 10-11 (newer northern): 48%. Districts 12-13 (Circle Mall vicinity): 45%. Districts 14 and southern: 38%. Premium branded buildings (all districts): 52%.

Cross-referenced against Property Finder market data and the Dubai Land Department transaction database, the figures broadly match the broader market consensus. JVC has delivered solid but not exceptional performance, with the best results concentrated in newer northern districts and premium branded buildings.

For yield-focused investors, older Districts 1-5 studios and one-bedrooms deliver the highest gross yields. For investors prioritising balanced returns, Districts 10-13 mid-tier units are the value sweet spot. For investors wanting capital growth ahead of yield, the premium branded buildings have delivered the strongest appreciation.

Should You Still Buy Into JVC

Looking at all of this, the verdict on JVC investment in 2026 splits into categories.

For first-time Dubai property investors with budgets in the AED 500,000 to AED 1.5 million range, JVC remains one of the strongest entry points in the city. The combination of moderate entry prices, mature tenant pool, predictable yields, and deep secondary liquidity makes it a low-stress first investment. The mistake to avoid is treating JVC like the frontier opportunity it was five years ago. The easy gains are gone. The conventional gains are still real.

For yield-focused investors building a Dubai portfolio, JVC is a solid component but not the highest-yield option. JVC works as part of a portfolio that also includes higher-yield Dubailand stock or Discovery Gardens older buildings. As a single-area concentration, JVC’s yield advantage over the market has narrowed.

For investors looking for capital growth, JVC is no longer the right call. The area has matured. Capital growth is now more or less in line with the Dubai apartment market average rather than ahead of it. Dubai South, selected off-plan developments, and emerging master-planned areas offer better forward-looking growth at similar entry prices.

For investors who want a hybrid (decent yield, moderate growth, low operational complexity, deep tenant pool), JVC delivers that profile better than almost any other Dubai apartment district in 2026. The unsexy but reliable mid-tier proposition is the current JVC story.

Building selection matters more in JVC in 2026 than it did three years ago, because the variance between best-performing and worst-performing buildings within the same district has widened as the area has matured. The Belgravia, Bloom, and similar premium mid-tier buildings consistently outperform the generic supply. Older buildings need careful inspection. Off-plan launches need developer track record verification.

For anyone considering specific buildings or units, the team can pull live yield data, void rate history, service charge trajectory, and resale comparables. The variance across JVC and adjacent Dubai mid-tier areas is wide enough that the building selection genuinely matters as much as the area selection. Our agents handle JVC transactions regularly, and current off-plan launches in JVC and similar districts often include attractive payment terms. Ready to look at specific units? Reach out and we’ll take it from there.

.svg)