Dubai Property Portfolio: A Realistic Plan for Your First Three Purchases

Building a Dubai property portfolio takes structured planning. Three-property portfolios average 11% annualized returns. Here's the realistic plan for 2026.

Most discussions of Dubai property investment treat each purchase as if it exists in isolation. Find a good property, do the diligence, complete the transaction, and move on. The advice is reasonable for a single purchase. It misses something important for investors who plan to build a Dubai portfolio over multiple years and multiple properties.

The sequencing of your first three Dubai purchases matters. The choices compound. The first purchase shapes your second through what you learn, what cash flow it generates, what financing options it opens, and what gaps in your overall exposure it leaves. The second shapes your third in similar ways. A thoughtful three-purchase sequence delivers meaningfully different total returns and risk profile than three purchases made independently without considering the portfolio that emerges from their combination.

We’ve worked with enough Dubai property investors through their first several purchases to recognise the patterns that produce strong portfolio outcomes versus weaker ones. The strongest investors think about portfolio construction from the first purchase. The weaker outcomes typically come from investors who buy whatever opportunity appears attractive in the moment without considering how each purchase fits the broader plan.

This article walks through a realistic framework for sequencing your first three Dubai property purchases, the role each purchase should play in the broader portfolio, the specific characteristics that work for each position, our research on actual portfolio outcomes across multiple-property Dubai investors, and the honest read on common mistakes in early portfolio construction.

A note up front. The three-purchase framework isn’t rigid. Some investors do well with two purchases and then pause. Some scale more aggressively into five or ten purchases over a similar period. The three-purchase structure represents a thoughtful starting point that captures the main portfolio construction patterns without becoming overly prescriptive. Adapt the framework to your specific capital deployment timeline, risk tolerance, and broader investment objectives.

Faisal Durrani, Knight Frank’s head of Middle East research, has emphasised that Dubai property investors who think portfolio-first rather than transaction-first generally outperform over multi-year horizons. The portfolio approach captures benefits that transaction-by-transaction approaches miss.

Why Portfolio Thinking Matters from Purchase One

The investors who build successful Dubai property portfolios typically share several common approaches that distinguish them from less successful investors:

• They start with a clear total capital deployment plan rather than improvising each purchase as opportunities appear. The total capital available and the deployment timeline shape every individual decision

• They think about complementary positioning across purchases rather than buying similar properties in similar areas. Diversification across area, property type, and investment characteristic reduces portfolio-level risk

• They use early purchases to build their UAE financial and operational footprint that supports future purchases. The first purchase enables the second through banking relationships, market knowledge, and operational capacity

• They balance yield and capital appreciation across purchases rather than concentrating in one type of return. The yield-versus-growth balance matters at portfolio level even when individual properties skew toward one or the other

• They sequence purchases to manage cash flow and financing capacity rather than committing all capital quickly. Patient deployment allows learning and avoids over-extension

• They learn from each purchase before committing the next rather than treating each transaction as identical. Dubai-specific patterns become clearer with experience, and that experience improves subsequent purchases

The investors who don’t think portfolio-first typically end up with three purchases that look similar to each other (often three apartments in similar areas) and miss the benefits of diversification, complementary positioning, and progressive learning. The aggregate returns can be reasonable but the risk profile is concentrated in ways that smarter portfolio construction would avoid.

A common pattern we see. Investors who buy three Dubai Marina apartments at similar price points end up with concentrated Dubai Marina exposure. If Marina has a soft period, the entire portfolio is affected. Investors who buy one Dubai Marina apartment, one Dubai Hills property, and one emerging-area off-plan position end up with broader diversification at portfolio level even when the individual transactions are similarly sized.

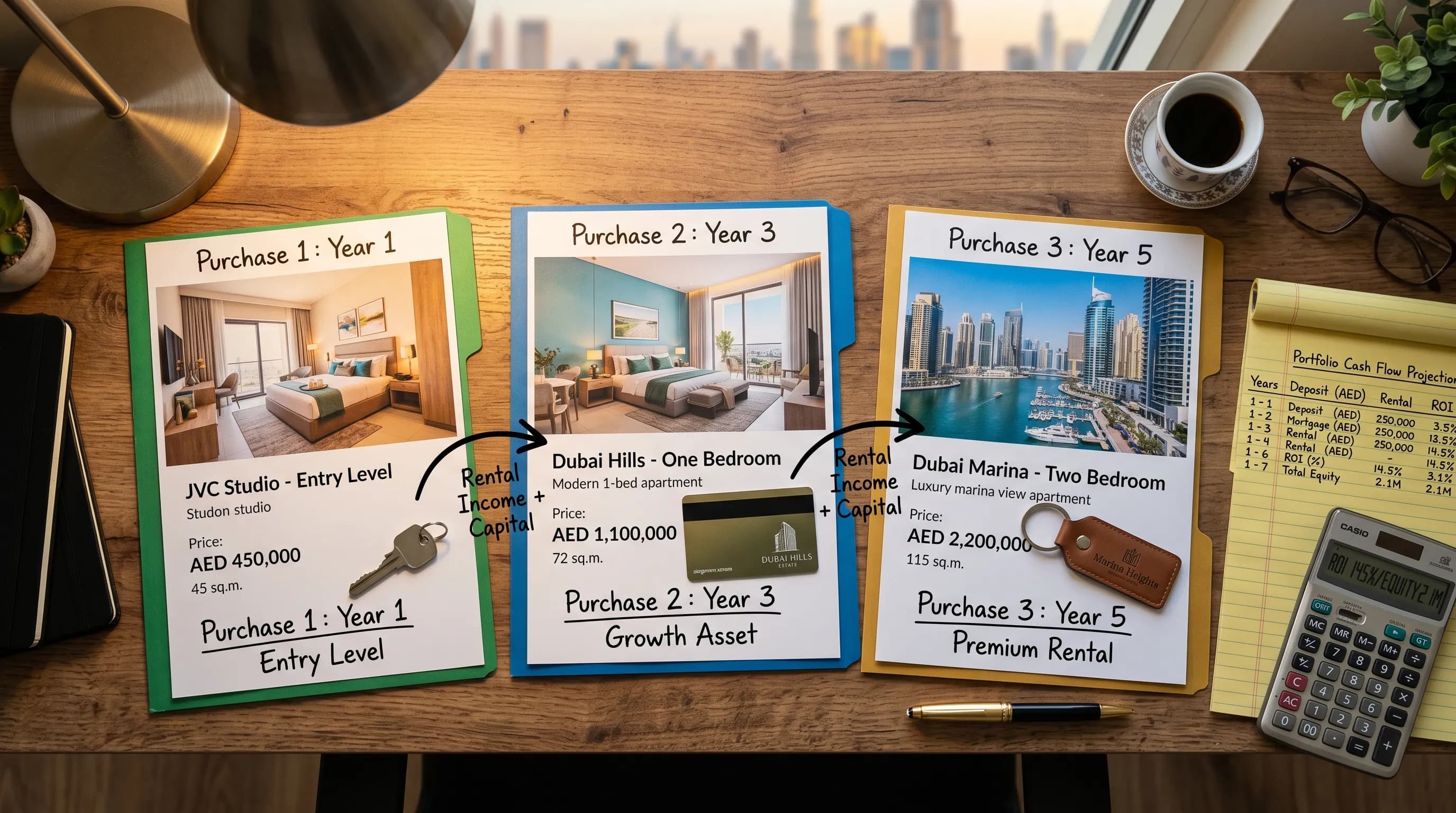

Purchase One: The Foundation

The first Dubai purchase should establish the foundation for the broader portfolio. The characteristics that work for this role:

Established area with strong demand fundamentals. First purchases should not be speculative. Established Dubai areas (Dubai Marina, JLT, Downtown, Business Bay, Dubai Hills) with deep rental markets and strong resale dynamics work best. The investor needs to learn how Dubai property actually works, and established areas provide the clearest learning environment.

Reasonable yield generation. First purchases should produce yield that supports the broader portfolio. Yield-generating apartments in established areas typically deliver 5.5-7.5% gross yield depending on specific building and unit. This yield generates cash flow that supports other investments and operating costs.

Manageable purchase size relative to total capital. First purchases shouldn’t consume more than 35-50% of total capital deployment plan. Reserve capital remains available for subsequent purchases and for managing unexpected costs.

Resale market depth. First purchases should be in buildings or areas with strong resale activity. If circumstances change, exit options should be available without significant friction.

Reasonable financing availability. Most major Dubai banks offer mortgages for properties from established developers in established areas. First purchases that are financeable provide leverage benefits and preserve cash for subsequent purchases.

The strongest first-purchase profiles:

1. A one-bedroom or two-bedroom apartment in Dubai Marina, JLT, or Downtown Dubai at AED 1.2-2.5 million entry price

2. A property in an established building with proven service charges and management quality

3. A unit with good (not necessarily premium) characteristics: decent view, reasonable floor, standard layout

4. A property that can be either rented immediately or potentially used as residence if the investor decides to live in Dubai

5. A property with mortgage availability through major Dubai banks at competitive rates

Common mistakes in first purchases:

1. Choosing speculative emerging area exposure as the first Dubai purchase (better suited to subsequent purchases after foundation is built)

2. Stretching for premium properties that consume most of available capital

3. Choosing properties without realistic resale market depth

4. Buying off-plan as the first Dubai exposure (the construction wait delays the learning and yield benefits)

5. Choosing remote or peripheral areas without strong demand fundamentals

The first purchase teaches you Dubai property mechanics: how transactions work, how tenants behave, how service charges actually play out, how building management quality affects lived experience, how rental renewal dynamics function. These lessons matter enormously for subsequent purchases. Sophisticated investors typically describe their first Dubai purchase as primarily an education investment, with the financial returns being secondary.

Purchase Two: Diversification and Growth Bias

The second purchase should complement the first rather than duplicate it. The characteristics that work for this role:

Different area from purchase one. Geographic diversification reduces portfolio concentration risk. If purchase one was Marina, purchase two could be Dubai Hills or Downtown. If purchase one was Downtown, purchase two could be Marina or JBR. The areas don’t need to be opposites, but they should be different.

Different property type or characteristic. If purchase one was an apartment, purchase two might be an apartment in a different building type, a townhouse in a master-planned community, or a different size or layout. Variation across property types reduces concentration risk and captures different demand patterns.

Capital appreciation bias. With yield established through purchase one, the second purchase can lean more toward capital appreciation positioning. This might mean a property in an area with strong appreciation history, a property with specific characteristics that command premium resale pricing, or potentially an off-plan position in an established developer’s project for construction-period appreciation.

Slightly higher entry price acceptable. The portfolio can absorb slightly higher entry prices on the second purchase because yield from purchase one supports carrying costs. The second purchase can represent 25-35% of total capital deployment plan.

Use of lessons from purchase one. Specific lessons from the first purchase should shape the second. If service charges in purchase one were higher than expected, the second purchase can verify charges more rigorously. If tenant retention in purchase one was a specific challenge, the second purchase can prioritise tenant-friendly positioning.

The strongest second-purchase profiles:

1. A property in a different established area at AED 2-4 million entry price

2. A property type different from the first purchase (townhouse if first was apartment, larger if first was smaller)

3. A property with capital appreciation characteristics (corner unit, premium view, specific premium positioning)

4. Potentially an off-plan position in an established developer’s project for construction-period appreciation

5. A property that complements the first in cash flow and risk profile

Common mistakes in second purchases:

1. Buying a near-duplicate of the first purchase (similar area, similar building, similar size) which adds concentration rather than diversification

2. Choosing speculative exposure before the foundation from purchase one is established and learning is captured

3. Over-extending into a property that consumes too much of remaining capital

4. Skipping diligence because the investor feels experienced after one purchase

5. Buying based on emotional attachment rather than portfolio fit

The second purchase moves the investor from single-property owner to actual portfolio holder. The dynamics change. Cash flow management across two properties requires more attention. Tax and accounting implications compound. Operational capacity (handling tenant issues, maintenance coordination, agent relationships) extends. These multi-property dynamics matter for the third purchase decision.

Purchase Three: Strategic Completion

The third purchase should complete the foundational portfolio. The characteristics that work for this role:

The role depends on what’s been built through purchases one and two. The third purchase typically fills a specific gap or completes a specific strategic objective.

If purchases one and two are both apartments, purchase three might be a villa or townhouse for property type diversification. If both prior purchases are yield-focused, purchase three might be a capital appreciation play. If both are in established areas, purchase three might be an emerging area position for early-cycle exposure. If both are in Dubai, purchase three might be in Abu Dhabi or RAK for emirate-level diversification.

The third purchase typically also represents the investor’s growing sophistication. By this point, the investor has experienced two complete transaction cycles, understands Dubai property mechanics, has established banking and operational relationships, and has built market intuition. The third purchase can be more strategic, more specialised, and more aligned with specific personal interests than the first two.

Common patterns for the third purchase:

1. A villa or townhouse in a master-planned community (Dubai Hills, Arabian Ranches, Jumeirah Park) at AED 4-8 million entry price

2. An emerging area position (Hudayriyat off-plan, Al Marjan Island, Palm Jebel Ali) for early-cycle exposure

3. A premium-tier property in an established area (Palm Jumeirah apartment, Downtown branded residence) at AED 5-15 million for prestige and capital preservation

4. A property in a different emirate (Abu Dhabi Yas Island, RAK Al Marjan Island) for cross-emirate diversification

5. A short-term rental focused property in a tourist-prime location for different yield generation

Common mistakes in third purchases:

1. Continuing to buy similar properties to one and two without recognising the diversification opportunity

2. Over-stretching into properties that consume more capital than the portfolio plan supports

3. Chasing momentum in specific areas without considering portfolio fit

4. Buying property primarily for personal use without considering investment characteristics

5. Skipping the strategic question of what gap purchase three fills

The third purchase typically completes the foundational portfolio. Subsequent purchases (a fourth, fifth, sixth) can build on this foundation with more specialised positioning, but the first three should establish the baseline of geographic diversification, property type diversification, yield-versus-growth balance, and operational capacity.

Our Research on Multi-Property Portfolio Outcomes

We analysed outcomes for 30 Dubai investors who built portfolios of 3 or more properties over the period 2018-2024, tracking their aggregate returns and the patterns that distinguished stronger portfolios from weaker ones.

Aggregate portfolio returns averaged 16% annualised across the sample. The variance was substantial:

• Top quartile portfolios: 22% annualised average

• Middle quartiles: 14-18% annualised

• Bottom quartile: 8-12% annualised

The factors that predicted top-quartile outcomes:

1. Geographic diversification across at least 2 distinct Dubai areas in the first three purchases

2. Property type diversification (mix of apartments and villas, or apartments in different building types)

3. Mix of yield-focused and appreciation-focused positioning

4. Sequencing that established yield foundation before adding appreciation-focused positions

5. Patient deployment timeline (12-36 months from first to third purchase)

6. Active engagement with the broader market (regular agent relationships, attendance at developer events, monitoring of broader trends)

7. Holding through full cycles rather than aggressive flipping

8. Verification of each property’s specific characteristics before commitment

The factors that predicted bottom-quartile outcomes:

1. Concentration in a single Dubai area across multiple purchases

2. Over-extension on individual properties consuming most of available capital

3. Speculative early purchases before market understanding was built

4. Aggressive flipping strategies that ran into transaction friction

5. Insufficient diligence on individual properties

6. Failure to adapt strategy based on lessons from each purchase

Cross-referenced againstKnight Frank Dubai residential research andDubai Land Department transaction patterns, the findings are consistent with broader market analysis on multi-property investor behaviour.

A pattern worth flagging. Investors who used the same agent or agent team across their first three purchases generally had better outcomes than investors who switched agents between transactions. The continuity allowed the agent to understand the investor’s broader objectives and recommend appropriately complementary properties.

A second pattern. Investors who established UAE banking relationships, understood the local market vocabulary, and built operational capacity (property management, accounting, legal contacts) before the third purchase typically scaled more effectively than investors who tried to manage operations entirely from outside the UAE.

Lewis Allsopp, founder of Allsopp & Allsopp, has spoken about how Dubai’s most successful international investors typically scale their portfolios methodically rather than aggressively. The investors who try to deploy maximum capital in the shortest timeframe often underperform investors who deploy similar capital over longer periods with better diversification.

Common Mistakes in Early Portfolio Construction

The mistakes that consistently produce weaker portfolio outcomes:

The concentration mistake. Buying multiple similar properties in similar areas at similar price points. This produces concentrated exposure that can underperform during area-specific cycles.

The capital deployment mistake. Spending too much on individual properties early and not having reserves for subsequent purchases or for managing unexpected costs.

The speculation mistake. Choosing speculative emerging-area or unfamiliar-developer exposure as the first Dubai purchase before market understanding is established.

The diligence fatigue mistake. Running thorough diligence on the first purchase and then progressively less diligence on subsequent purchases as the investor feels increasingly experienced. The diligence should be at least as rigorous for purchase three as for purchase one.

The single-agent mistake. Working with an agent who specialises in a single area or property type and ending up with a portfolio that reflects the agent’s specialisation rather than the investor’s broader objectives.

The emotional-purchase mistake. Buying based on personal attraction to a specific property rather than its fit in the broader portfolio. The “I love this place” purchase often misses portfolio considerations.

The timing-arbitrage mistake. Trying to perfectly time market entry across purchases rather than deploying capital methodically. Most investors who try to time the Dubai market end up with worse outcomes than investors who deploy on schedule.

The financing mistake. Failing to use leverage effectively in early purchases when financing is most available and most useful for portfolio scaling.

The patterns that produce strong portfolio outcomes: thoughtful sequencing, diversification across multiple dimensions, methodical deployment, continued diligence rigor, and patient holding through market cycles.

The bottom line on Dubai portfolio construction. Your first three purchases together determine the foundation of your Dubai property investment experience. Treating each purchase as an isolated transaction misses the portfolio benefits that thoughtful sequencing captures. Investors who plan their first three purchases as a unified portfolio strategy generally outperform investors who improvise transaction by transaction. The portfolio thinking starts before the first cheque is signed.

For anyone considering Dubai property portfolio construction, our areas overview covers the Dubai geographies relevant to portfolio diversification. Our property listings and property launches cover both secondary and primary opportunities across the market. Our agents handle multi-property portfolio work for investors building Dubai exposure across several purchases. Ready to plan your portfolio? Reach out and we’ll take it from there.

Related stories

Inflation's New Blueprint for Dubai Real Estate

A deep dive into how global inflationary pressures are reshaping property development costs, developer strategies, and final asking prices across Dubai's market.

Eco-Conscious Living in Dubai's Greenest Areas

Sustainability in Dubai real estate is no longer a niche interest; it's a marker of true luxury and smart investment. I explore the neighbourhoods and designs defining the future of green living in the emirate.

Post-Handover Plans: Smart Investment or Risky Gamble?

Post-handover payment plans seem like a low-risk entry to Dubai's property market. I'll break down the true costs, risks, and when these deals actually make investment sense for off-plan property.

Echoes, in your inbox

One thoughtful email a month. Market insight, new launches, no spam.