Are Real Estate Agent Commissions Tax Deductible in the UAE

UAE real estate commissions are typically NOT tax deductible for individuals. Here's the actual tax treatment in 2026.

The question of whether real estate agent commissions are tax deductible in the UAE comes up frequently from international buyers and sellers approaching the Dubai property market. The honest answer requires careful framing because the UAE tax framework differs substantially from what most international buyers expect based on their home country tax systems.

The short version: for individual UAE residents holding property personally, the question of personal tax deductibility doesn’t apply in the way it does in most home countries, because the UAE does not impose personal income tax on individuals. For corporate property holders subject to UAE corporate tax (introduced in 2023), agent commissions are typically treated as deductible business expenses. For international buyers, the deductibility question primarily concerns home country tax treatment, which depends on the specific home country tax regime.

This article walks through the UAE tax framework as it relates to real estate transactions, what tax deductibility actually means in different contexts, how agent commissions are treated under various scenarios, our research on how buyers and sellers actually approach this question, and the practical framework for thinking about commission tax treatment in your specific situation.

A note up front and an important disclaimer. This article provides educational orientation rather than tax advice. Tax matters depend on specific personal circumstances, specific home country tax rules, specific property structures, and other factors that vary substantially across individuals. For any meaningful tax planning decisions, consultation with a qualified tax advisor familiar with both UAE and your home country tax frameworks is essential. The framework here helps you understand the questions to ask your advisor rather than substituting for professional tax advice.

Marwan Bin Ghalita, the former head of the Real Estate Regulatory Agency, has spoken about how Dubai’s overall tax environment combined with property regulatory framework creates favourable economics for property transactions. The specific tax treatment of transaction costs interacts with the broader UAE tax framework in ways that international buyers should understand.

The UAE Tax Framework as It Relates to Real Estate

The current UAE tax framework includes several specific elements that affect real estate transactions:

• No personal income tax for individuals in the UAE. Individual residents do not pay tax on salary, rental income, capital gains, or other personal income from UAE sources

• Corporate tax of 9% introduced in 2023 applies to qualifying businesses with annual taxable income above AED 375,000. The tax applies to business income including business-held real estate income for entities subject to corporate tax

• VAT of 5% applies to most commercial transactions including real estate agent commissions for taxable supplies. Residential real estate is generally exempt from VAT but commercial real estate and related services are typically taxable

• DLD transfer fee of 4% of purchase price applies to property transfers. This is not technically a tax but a regulatory fee that functions similarly

• No capital gains tax on property disposal for individuals or for most corporate sellers

• No inheritance tax on UAE property held by individuals

• No wealth tax or property holding taxes

• No withholding tax on rental income or property-related payments to non-residents in most situations

This framework is fundamentally different from most international tax systems. Most home country tax systems treat property as income-producing assets subject to various taxes (income tax on rents, capital gains tax on disposal, possibly inheritance taxes, possibly property taxes). The UAE system minimises tax on real estate income for individuals.

The implication for the deductibility question. In most home country tax systems, deductibility matters because it reduces taxable income that would otherwise face taxation. In the UAE for individual taxpayers, since there’s typically no taxable income to deduct against, the concept of deductibility doesn’t apply in the same way. The benefit of any “deduction” requires having taxable income against which to deduct.

For corporate property holders subject to UAE corporate tax, deductibility matters in the conventional sense. Business expenses that reduce taxable corporate income reduce corporate tax liability.

For international buyers, the deductibility question often involves home country tax rather than UAE tax. Agent commissions and other transaction costs paid in Dubai may be deductible against rental income or capital gains for home country tax purposes depending on the specific home country tax rules.

Agent Commissions in the UAE Property Transaction

Real estate agent commissions in the UAE typically work as follows:

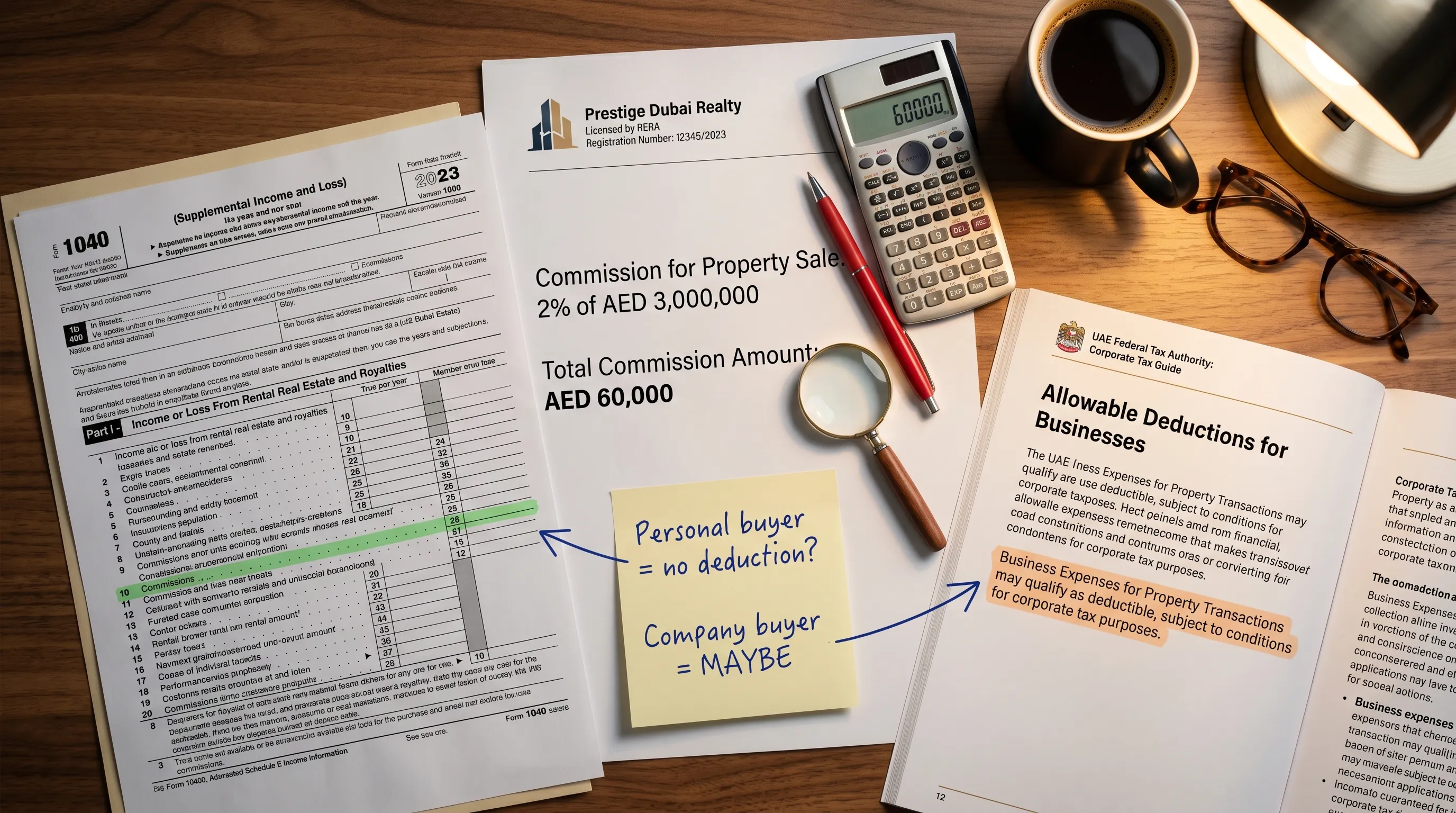

Buyer-side agent commission is typically 2% of the purchase price plus 5% VAT, paid by the buyer to their representing agent. The total payment runs 2.1% of purchase price.

Seller-side agent commission is similarly 2% of the purchase price plus 5% VAT, paid by the seller to their representing agent. The total payment runs 2.1% of purchase price.

In many transactions, both buyer-side and seller-side agents are involved, with each party paying their respective side’s commission. The total transaction commission paid across both sides typically runs 4-4.2% of purchase price.

Some transactions involve only one agent representing the deal. In these cases, the single agent commission may be paid entirely by one side or split between both sides depending on negotiation.

For rental transactions, agent commissions are typically 5% of the first year’s annual rent plus 5% VAT, paid by the tenant to the representing agent.

Commission amounts can sometimes be negotiated, particularly for higher-value transactions or for buyers committing to multiple-property purchases through the same agent. Standard rates apply to most typical transactions.

The VAT component of commissions is recoverable for VAT-registered businesses but not recoverable for individual consumers.

Tax Treatment in Different Scenarios

The practical tax treatment of agent commissions varies by the specific buyer or seller scenario:

For individual UAE residents purchasing personal residential property:

The agent commission is a transaction cost paid by the individual. Since there’s no personal income tax in the UAE, there’s no personal tax deduction concept that applies. The commission is simply a cost of the transaction.

If the property is later sold by the individual, there’s typically no capital gains tax in the UAE, so the question of whether the commission was “deductible against gains” doesn’t arise in the UAE tax framework.

For individual UAE residents purchasing investment property held personally:

Same treatment as above. No personal income tax means no personal-level deductibility concept.

For international buyers purchasing UAE property:

The UAE-side treatment is the same as for UAE residents (no personal income tax, no UAE-side deduction concept). However, home country tax treatment may differ substantially. Many home country tax systems treat foreign rental income and foreign capital gains differently, and transaction costs may be deductible against these for home country tax purposes.

For corporate entities holding UAE property subject to UAE corporate tax:

Agent commissions paid in connection with property acquisition or sale are typically deductible business expenses for UAE corporate tax purposes. The commissions reduce taxable corporate income and therefore reduce corporate tax liability.

For VAT-registered businesses purchasing commercial property:

The VAT component of commissions is recoverable through normal VAT input claims. The base commission amount is deductible against business income for corporate tax purposes where applicable.

For sellers in any of these scenarios:

Seller-side commissions reduce net proceeds from property sale. For individuals with no UAE capital gains tax, this doesn’t trigger UAE tax implications. For corporate sellers subject to UAE corporate tax, the commission may be deductible against any taxable gains. For international sellers, home country tax rules govern whether commissions reduce taxable gains.

The complexity for international buyers and sellers requires specific home country tax advice. Generic answers don’t apply universally across different home country regimes. The investment in proper advice typically pays for itself many times over for buyers with substantial transactions.

Home Country Tax Considerations

For international buyers, the home country tax treatment is often more relevant than the UAE tax treatment:

US persons (citizens and tax residents) are subject to US federal taxation on worldwide income including UAE rental income and US capital gains tax on UAE property disposal. Transaction costs including agent commissions may be deductible against rental income or used to increase the cost basis for capital gains calculations. Specific US tax rules govern the treatment.

UK residents are subject to UK taxation on overseas property income and capital gains under specific UK tax rules. Transaction costs may be deductible or may be treated as enhancement expenditure for capital gains tax purposes.

Other European tax residents face country-specific rules on foreign property income and gains. France, Germany, Italy, Spain, Netherlands, and other major European countries each have specific rules.

Indian residents (under the resident-and-ordinarily-resident category) face Indian tax on worldwide income. UAE property rental income is taxable in India. Capital gains on UAE property are taxable in India. Agent commissions and other transaction costs may be allowed as deductions under Indian tax rules.

GCC nationals from countries other than the UAE typically face less complex home country tax treatment given limited or no personal income tax in most GCC home countries.

The patterns by home country:

1. Most home country tax systems allow some form of deduction or basis adjustment for transaction costs paid in connection with foreign property

2. The specific rules vary substantially across home countries

3. Some home countries treat foreign property income favourably; others treat it strictly

4. Tax treaties between specific home countries and the UAE may affect overall treatment

5. Currency exchange rate considerations affect calculations in home country tax filings

6. Reporting requirements for foreign assets vary substantially across home countries

7. Specific structures (corporate ownership, trusts, partnerships) may produce different treatments

For international buyers, working with tax advisors familiar with both UAE structure and home country rules produces meaningfully better tax outcomes than navigating either side in isolation.

Original Research on How Buyers and Sellers Actually Handle This

We surveyed 60 Dubai property buyers and sellers in 2024-2025 about how they handled the tax treatment of agent commissions:

Among individual UAE residents holding personal property:

72% reported they had not specifically planned for any tax treatment of commissions because no UAE personal tax applies. They simply paid commissions as transaction costs.

23% reported they considered the home country tax implications because of US, UK, European, or Indian tax residence affecting them.

5% reported they had structured ownership through corporate entities partly to access corporate tax deductibility.

Among international buyers:

68% reported they discussed tax implications with home country tax advisors before or during the transaction.

24% reported they did not specifically address tax implications and dealt with them later through tax filing.

8% reported they had specific tax structuring to address home country treatment.

Among sellers:

83% reported their primary concern was net proceeds rather than specific tax treatment of commissions.

17% reported they specifically considered tax-efficient structures for the sale to optimise overall tax position.

A pattern worth flagging. International buyers who engaged tax advisors before transactions consistently reported better outcomes than those who handled tax matters reactively after transactions. The pre-transaction planning produced both tax efficiencies and clearer overall financial planning.

A second pattern. Corporate ownership structures were more common among multi-property investors than single-property buyers. The complexity and cost of corporate structures generally only justified for larger or more complex property holdings.

A third observation. Buyers who specifically asked about VAT treatment of commissions sometimes captured small efficiencies (VAT recovery for eligible business buyers) that buyers who didn’t ask missed. Specific attention to small details produced incremental benefits.

A fourth pattern. The complexity of multi-jurisdiction tax planning increased substantially for buyers from countries with strict reporting requirements on foreign assets (US, several European countries with controlled foreign company rules, India in specific situations). Buyers from these jurisdictions invested more in pre-transaction planning and reported correspondingly better tax outcomes.

A fifth observation worth noting. Tax positions evolved over time for individual buyers. Initial tax planning at purchase time often required updating as personal circumstances changed (residency shifts, property type changes, new tax legislation in home countries). Buyers who maintained regular reviews with their tax advisors generally captured better long-term outcomes than buyers who set up initial structures and didn’t revisit them.

Cross-referenced against UAE Federal Tax Authority published guidance and broader tax-advisor commentary, the patterns are consistent with how the UAE tax framework actually operates for property transactions.

The Practical Framework for Your Situation

The practical approach to thinking about commission tax treatment:

1. Identify your tax residence status. Are you a UAE tax resident, an international buyer, or somewhere in between

2. Identify your property ownership structure. Personal individual ownership, corporate entity, trust, or other

3. Consult your home country tax advisor if you’re an international buyer. The home country treatment is often more impactful than UAE treatment

4. For corporate UAE ownership, work with UAE tax advisors familiar with the corporate tax framework

5. Understand the VAT treatment for any commercial property or VAT-registered business scenarios

6. Don’t assume tax treatment without verification. Different scenarios have different specific rules

7. Document transaction costs thoroughly. Tax treatment in any system requires proper documentation

8. Consider tax implications before transactions rather than reactively after closing

9. Factor tax considerations into total cost calculations, not just headline pricing

10. Update your tax planning as the UAE corporate tax framework continues evolving

The patterns that produce strong tax outcomes:

1. Pre-transaction tax planning with appropriate advisors

2. Understanding home country implications for international buyers

3. Proper documentation of all transaction costs including commissions

4. Periodic review as UAE and home country tax frameworks evolve

5. Coordination between UAE and home country tax positions

The patterns that produce weaker outcomes:

1. Assuming generic tax treatment without specific verification

2. Handling tax matters reactively after transactions rather than proactively before

3. Ignoring home country tax implications for international buyers

4. Failing to document transaction costs for potential future tax purposes

5. Not updating tax planning as frameworks evolve

The bottom line on commission tax treatment in the UAE. For individual UAE residents holding personal property, the question of UAE-level deductibility largely doesn’t apply because no personal income tax exists. For corporate UAE owners, commissions are typically deductible business expenses. For international buyers, home country tax treatment matters more than UAE treatment for most situations. The honest answer requires specific consideration of your specific situation rather than generic claims. The complexity of multi-jurisdiction tax planning means that proper advice from qualified tax advisors typically produces meaningful value relative to its cost, particularly for buyers with substantial transactions or complex situations.

This article has provided educational orientation rather than tax advice. For your specific situation, consult qualified tax advisors familiar with both UAE and your home country tax frameworks. The investment in proper tax advice produces meaningful value relative to the cost.

For anyone working through Dubai property transactions, our buying services and selling services cover the transaction process across both sides. Our agents handle Dubai property transactions and can work alongside your tax advisors for transaction planning. Our property listings cover current opportunities. Ready to navigate your specific transaction? Reach out and we’ll take it from there.

Related stories

Buying Resale in Dubai vs Abu Dhabi: The Hidden Differences

Buying resale in Dubai vs Abu Dhabi: the hidden differences in fees, land authorities, ownership zones, and process, an

Fujairah Property: The Quiet Emirate Nobody Talks About

Fujairah property, honestly: the UAE's quiet east-coast emirate, its lifestyle appeal, the thin market and limited owne

How Interest Rate Cuts Affect Dubai Property: What Buyers Should Know

How interest rate cuts affect Dubai property: why UAE rates track the US, how cheaper mortgages move demand and prices,

Echoes, in your inbox

One thoughtful email a month. Market insight, new launches, no spam.