The True Cost of Renting Long-Term vs Buying in Dubai Over a Decade

The true cost of renting long-term vs buying in Dubai over ten years: rent, mortgage, fees, equity, and opportunity cos

The conventional wisdom goes something like this: Rent is wasted capital, therefore buy. Although this might seem obviously true, the truth about what happens over the course of a decade is not so straightforward. What matters is not which seems to make more sense, but the true cost of each in light of everything.

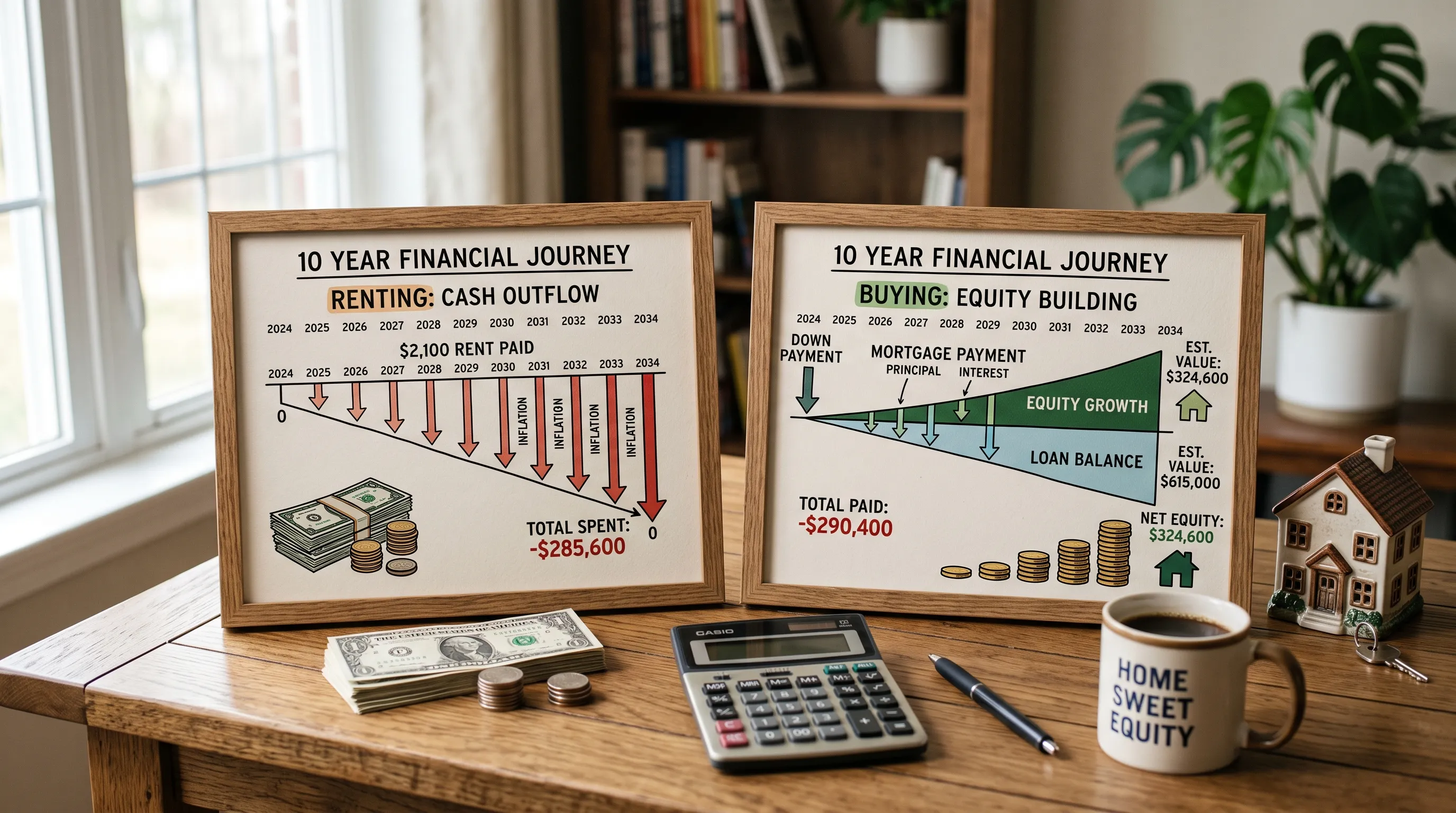

That is the crux of how to compare the true cost of renting versus buying in Dubai over a decade, in other words not just how much you would save on rent compared to buying and building up equity, but a true comparison of total rental costs as they increase over ten years versus total buying costs which include upfront fees, mortgage interest, charges and maintenance, less the equity build-up and any gains in the value of the property. With the opportunity cost of the money invested added into the equation, the true cost comparison begins to emerge.

The hard truth is that, assuming the homeowner stays put and prices do not fall, buying will come out ahead because of the accumulation of equity along with higher rent. But that is not certain; prices can fall, the homeowner may have to move, and that money could have been used in some other way. There is no clear winner except for what the numbers show in relation to the individual situation.

Here is what the guide covers in detail: the true cost of renting, the true cost of buying, comparison of costs over ten years, how “dead money” can be an oversimplification, and an honest assessment of which one comes out better.

First of all, the straight talk about where we stand. We are engaged in both buying and renting properties, and we admit the possible conflict of interest. We tried to be relatively unbiased in this information, which is general information only, not financial advice. The numbers are just examples, and there are no predictions as to what prices will do over the next few years, which is impossible anyway. With that in mind, here is the comparison of true cost that is based on the facts.

The True Cost of Renting

Start with renting, and be fair to it, because it gets an unfairly bad name. The rent you pay over ten years is a large sum, and it is true that none of it builds equity, so at the end you own nothing. It is also true that rent tends to rise over time, within Dubai's regulated increases, so the cost usually climbs across the decade rather than staying flat.

But that is only half the picture. Renting has no big upfront cost beyond a deposit and fees, so the capital you would have sunk into a purchase stays free to invest elsewhere, which is a real and often ignored benefit. You carry no service charges or major maintenance, since the landlord does, and you keep full flexibility to move, change areas, or leave the country without the cost and hassle of selling. For current rent levels and the regulated increase index, the Dubai Land Department is the reference.

That flexibility is easy to undervalue until you need it. A job change, a growing family, a move back home, or simply a better deal a few streets away, a renter can act on all of those quickly and cheaply, while an owner has to sell first, which takes time and costs money. Our rental service works across the market if renting is your route.

Here is the true cost of renting:

- Total rent paid. A large sum with no equity built.

- Rising over time. Rent tends to climb across a decade.

- No big upfront cost. Just a deposit and fees.

- Capital stays free. To invest or use elsewhere.

- No maintenance burden. The landlord carries the big costs.

- Full flexibility. Move or leave without selling.

The honest summary is that renting costs you the rent, which rises and builds no equity, but it frees your capital, spares you maintenance and service charges, and keeps you flexible. Those benefits have real value that the dead-money slogan ignores. Whether renting is the cheaper path over ten years depends entirely on what buying would have cost and done over the same time, which is the other half of the sum, and where most people stop thinking too early.

The True Cost of Buying

Now buying, which has more hidden cost than the equity story suggests. The upfront hit is the first shock, a deposit of roughly a fifth to a quarter of the price for expats under the lending rules, plus a land department transfer fee of around 4%, an agency fee of about 2%, and mortgage and valuation fees, so on a home of, say, AED 1.5 million you are finding a large sum before you move in, much of it, the fees, gone for good. Our mortgage team can lay out the real upfront numbers for a given purchase.

Then come the ongoing costs. A big share of your early mortgage payments is interest, which is a cost, not equity, just like rent, and only the principal portion builds your stake. On top sit annual service charges, maintenance, and insurance, real recurring money that renting avoids, and our property management team sees how much those add up to over the years. At the end you own equity, the principal you have paid down plus or minus whatever the property has done in value, and if you sell you pay selling costs too.

Here is the true cost of buying:

- Heavy upfront. Deposit, transfer fee, agency fee, and mortgage costs.

- Sunk fees. The transfer and agency fees do not come back.

- Interest is a cost. Early payments are mostly interest, not equity.

- Ongoing charges. Service charges, maintenance, and insurance.

- Equity built. Principal paid down over the years.

- Price exposure. Value can rise or fall, and neither is promised.

The honest summary is that buying builds equity, but it is not free of dead money, since interest, transaction fees, service charges, and maintenance are all real costs that do not add to your stake. The equity and any price gain are the payoff, but the gain is never guaranteed, so the honest way to weigh buying is on the costs you can be sure of, treating any appreciation as a bonus rather than the plan. That is the mistake to avoid, banking on a rise nobody can promise.

Renting vs Buying in Dubai Over Ten Years

So over a decade, which actually costs less? The honest answer is that buying often wins, but only under conditions, and never guaranteed. Buying tends to come out ahead over ten years when you stay put the whole time, so the big upfront fees spread thinly across the decade, when prices at least hold their value, and when your mortgage cost is not wildly above the rent you would have paid. In that common case, you build equity while a renter builds none, and rising rent works against renting while your mortgage is steadier.

But the conditions matter, and renting can win. If prices fall or stagnate over the decade, the equity story weakens or reverses. If you move within a few years, the transaction costs never amortise and buying loses. And if the deposit you tied up could have earned a strong return invested elsewhere, that opportunity cost can tip the maths toward renting. The lending rules that set your deposit and borrowing sit with the Central Bank of the UAE, and they shape how much capital buying locks up in the first place.

Here is the ten-year read:

- Buying often wins if you stay. Fees spread over the decade.

- And if prices hold. Equity plus stability beat rising rent.

- Renting can win if prices fall. The equity case weakens.

- Or if you move early. Transaction costs never amortise.

- Or on opportunity cost. If the deposit earns more elsewhere.

- Never guaranteed. It depends on your numbers, not a rule.

The honest summary is that over ten years buying frequently beats renting on cost, but only if you stay, prices hold, and the numbers stack up, and renting can absolutely win if any of those fail. There is no universal answer, because the result hinges on things that vary, how long you stay, what prices do, and what your capital could earn, and one of those, the price, nobody can predict. So the right move is to run your own decade with honest, conservative assumptions rather than trusting the slogan. A good discipline is to run it twice, once assuming prices stay flat and once assuming a modest fall, and see whether buying still holds up, because a decision that only works if prices rise is a bet, not a plan.

It's Not About Dead Money

The dead-money idea deserves a proper burial, because it misleads people on both sides. Renting is not pure waste, since it buys you flexibility, frees your capital, and spares you maintenance, all of which have real value. And buying is not pure saving, since a big chunk of it, the interest, the fees, the service charges, the maintenance, is money that never becomes equity, exactly the dead money renters are warned about. Both paths have costs that vanish and costs that build.

Once you drop the slogan, the decision becomes clearer and more personal. It is really about three things, how long you will stay, how you weigh flexibility against stability, and whether you can carry buying comfortably without stretching. A long, settled stay favours buying. A likely move or a love of flexibility favours renting. And buying only makes sense if you can afford it within your means, since an overstretched purchase is worse than a comfortable rental every time. The wider picture on living and settling in the country sits within the UAE government portal.

Here is the clearer way to see it:

- Renting is not pure waste. It buys flexibility and frees capital.

- Buying is not pure saving. Interest and fees are dead money too.

- Length of stay matters most. Longer favours buying.

- Flexibility has value. Hard to price, but real.

- Stability has value too. A settled home is worth something.

- Affordability rules all. Never stretch to buy.

The honest summary is that neither renting nor buying is simply throwing money away, both mix dead money with value, so the real question is which mix fits your life, your timeline, and your budget. Answer how long you will stay, how much you value flexibility, and what you can comfortably afford, and the true-cost comparison stops being a slogan and starts being a decision you can actually make. That is a far more useful frame than dead money ever was.

The Honest Scorecard

So how do renting and buying compare over a decade, factor by factor? We scored it straight, each on one line:

- Rent over ten years: a large sum with no equity, and it usually rises over time.

- Buying upfront: heavy, with deposit, transfer fee, agency fee, and mortgage costs.

- Mortgage interest: a real cost, especially early, that does not build equity.

- Equity: buying builds it through principal, while renting builds none.

- Ongoing costs: buying adds service charges and maintenance that renting avoids.

- Price movement: uncertain, and never to be assumed either up or down.

- Opportunity cost: the deposit could earn elsewhere if you rented instead.

- The verdict: buying often wins over a decade if you stay and prices hold, not always.

The pattern is that buying's advantage is real but conditional, resting on staying long enough to amortise the fees and on prices at least holding, while renting's advantages, flexibility and free capital, are certain but quieter. Strip out the guesswork about prices, which nobody controls, and the decision comes down to your timeline and your comfort with the costs and the commitment.

Read the list and the honest takeaway is that this is not a contest with a fixed winner. For a settled buyer who will stay a decade and can afford it, buying usually costs less over the period and leaves them with an asset. For someone who might move, values flexibility, or would be stretched by the purchase, renting is often the smarter and safer path. Both are rational, and the numbers, not the slogan, decide which is yours.

The honest summary of the scorecard is that over ten years buying tends to win on cost when you stay and prices hold, renting tends to win on flexibility and certainty, and the right choice depends on your own timeline, budget, and tolerance for the risks buying carries. Run your decade with conservative numbers, weigh the flexibility you would give up, and choose on your situation rather than on what everyone says you should do.

What We Would Actually Do

Overall, the real comparison of cost between renting and buying in a decade-long span is not what the simple slogan says. Both of these choices mix up money going down the drain and money growing up. Buying usually becomes cheaper and provides an asset within the decade if you plan to stay, have good prices and can afford it, while renting works better when you may need to move somewhere else, prices are going down or if your money can be used for better purposes. There is always no simple answer here.

If our friend came and asked us which way he should choose, we would not give him any answer according to some catchy slogans and would ask three questions instead: How long are you going to stay? How important for you is the freedom of movement? Can you afford the purchase? Long staying in one place and being able to afford the house are signs of buying a property.

Then we would try to create the decade in both cases using conservative numbers. Think about the total of the rising rent in case of renting and about the expenses on the deposit, commissions, interest, service charge, and maintenance in case of buying, subtract the equity and think that there will be no price growth in the course of the decade – thus any profit will be bonus. This customized, data-driven comparison, calculated with your own figures, wins any rules of thumb.

The most frequent error that people make is buying due to the rent being dead money without thinking about dead money in buying, without considering whether you will stay long enough to justify the purchase and buying with stretched budget. Do a fair evaluation of both decades, do not rely on price increase, buy only if you can afford it and think of lost opportunities. If you act this way, either option will suit you perfectly.

If you want help modelling the true cost either way, or finding the right home if buying makes sense, that is exactly what we do. Our property buying service can run the real numbers alongside the rental alternative.

And if you want a straight, unbiased conversation about which path fits your decade, we are glad to help. Get in touch and we will take it from there.

Related stories

Buying Resale in Dubai vs Abu Dhabi: The Hidden Differences

Buying resale in Dubai vs Abu Dhabi: the hidden differences in fees, land authorities, ownership zones, and process, an

Fujairah Property: The Quiet Emirate Nobody Talks About

Fujairah property, honestly: the UAE's quiet east-coast emirate, its lifestyle appeal, the thin market and limited owne

How Interest Rate Cuts Affect Dubai Property: What Buyers Should Know

How interest rate cuts affect Dubai property: why UAE rates track the US, how cheaper mortgages move demand and prices,

Echoes, in your inbox

One thoughtful email a month. Market insight, new launches, no spam.